· AtlasPCB Engineering · Industry News · 7 min read

China Electronics Manufacturing Profits Surge 104% in H1 2026: Impact on PCB Pricing and Capacity

China's major electronics manufacturers report a 103.9% year-over-year profit surge in early 2026, driven by AI server demand and export growth. Analysis of how this boom affects PCB supply chain pricing, lead times, and capacity allocation for international customers.

The Numbers: What Just Happened

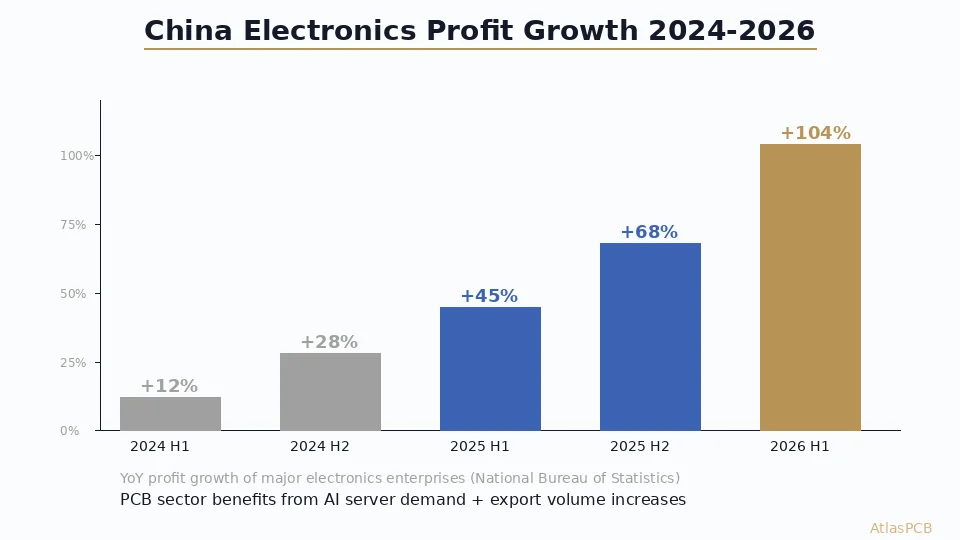

China’s National Bureau of Statistics reported that major electronics manufacturing enterprises posted a 103.9% year-over-year profit increase in the first half of 2026 — effectively doubling their earnings compared to the same period in 2025. This caps a remarkable acceleration that saw growth climb from 12% in H1 2024, through 28% in H2 2024 and 68% in H2 2025, to the current triple-digit surge.

The drivers are not subtle. The AI infrastructure buildout — from hyperscale data centers to edge inference deployments — has created unprecedented demand for advanced electronics manufacturing. Taiwan, whose semiconductor ecosystem is deeply intertwined with China’s electronics manufacturing base, recorded 51.7% export growth in May 2026, almost entirely attributable to AI infrastructure components. India has emerged as the third-largest electronics goods exporter, adding further demand pressure on component supply chains that PCB manufacturers share.

For hardware engineers and procurement teams outside China who rely on Chinese PCB fabrication, the question is straightforward: what does this boom mean for your pricing, lead times, and capacity access?

Direct Impact on PCB Supply Chain

Material Pricing: Copper-Clad Laminates Under Pressure

The PCB fabrication chain begins with copper-clad laminate (CCL), and the current demand environment has tightened supply across all grades. Standard FR-4 laminate pricing has increased 3-5% year-over-year — modest in isolation but compounding on already-elevated post-pandemic levels. The more significant pressure is on specialty materials:

Low-loss laminates (Megtron 4/6, Panasonic R-5775N) used in AI server motherboards and high-speed networking equipment have seen 8-12% price increases with extended lead times (4-6 weeks versus the historical 2-3 weeks). These materials compete directly with orders from PCB manufacturers building boards for hyperscale data center programs, where purchasing power and volume commitments give large OEMs preferential allocation.

Rogers high-frequency materials (RO4350B, RO4003C) remain relatively stable in pricing (+3-5%) because they serve different end-markets (RF, aerospace, automotive radar) that are not experiencing the same explosive demand as AI computing. For engineers building RF PCBs, the current environment is actually favorable — manufacturers have available Rogers material inventory while their AI-focused competitors are scrambling for low-loss laminates.

Copper foil — the other critical raw material — is tracking broader commodity markets with prices volatile above $6.10/lb. PCB manufacturers have largely absorbed this through supply agreements, but continued elevation will eventually pass through to board pricing, particularly for heavy-copper designs (3oz+) where material represents a larger fraction of total cost.

STABLE PRICING, COMMITTED SUPPLY

Dedicated Capacity for Export Customers

We maintain material inventory and reserved production slots for international engineering teams. No surprise pricing changes mid-order.

Get Current Pricing ›Capacity Allocation: The Real Concern

The profit surge tells us that Chinese electronics manufacturers are not just busy — they are profitable. This distinction matters for smaller customers. When a PCB fabricator is operating at 85-95% capacity utilization and choosing between a 10,000-panel AI server order at premium margins versus a 50-panel prototype run from an overseas startup, the allocation decision is obvious from a business perspective.

We are observing this dynamic across the industry in 2026. Large fabricators who previously competed aggressively for export business have raised minimum order values or extended quoted lead times for standard-complexity work, effectively de-prioritizing lower-margin orders without explicitly refusing them. The 3-5 day prototype lead time that was standard in 2024 has stretched to 5-7 days at some facilities simply because production scheduling prioritizes higher-value slots.

The counterpoint is that China’s PCB manufacturing base is enormous — over 2,800 fabrication facilities by some counts. The capacity squeeze is real only in the advanced segment (HDI, high-layer-count, specialty materials). Standard PCB fabrication (2-6 layers, FR-4, standard features) remains highly competitive with ample available capacity from mid-tier manufacturers. The market is bifurcating: premium capabilities are getting more expensive and harder to access, while standard capabilities remain available and price-competitive.

Lead Time Implications by Board Type

Based on our production data and industry observations, here is the current lead time landscape compared to 12 months ago:

| Board Type | Lead Time (July 2025) | Lead Time (July 2026) | Change |

|---|---|---|---|

| 2-layer FR-4 prototype (5-10pcs) | 3-5 days | 3-5 days | Stable |

| 4-layer FR-4 production (100+ pcs) | 7-10 days | 7-12 days | +1-2 days |

| 8-layer standard | 10-14 days | 12-16 days | +2-3 days |

| 10-14 layer with specialty material | 14-18 days | 18-25 days | +4-7 days |

| HDI (any buildup) | 14-21 days | 18-28 days | +4-7 days |

| Rogers RF boards | 12-18 days | 14-20 days | +2-3 days |

The largest extensions are in the 10+ layer and HDI segments — precisely where AI server boards compete for manufacturing resources. Standard boards remain largely unaffected.

PRIORITY SCHEDULING

Guaranteed Slot Reservations for Complex PCBs

Advance booking secures your production slot even during peak demand periods. Ask about our quarterly capacity planning program.

Reserve Production Slot ›What This Means for Your Sourcing Strategy

Short-Term (Q3-Q4 2026)

The boom shows no signs of cooling. AI capital expenditure from hyperscale companies continues to accelerate, and the downstream PCB demand follows directly. For the next 6-12 months, expect:

- Continued 3-5% price increases on standard materials, 8-15% on specialty

- HDI and high-layer-count lead times remaining 1-2 weeks extended

- Material availability for low-loss laminates requiring advance ordering (4-6 weeks)

- Smaller manufacturers competing aggressively for business displaced from large shops

Practical Recommendations

For engineers and buyers navigating this environment, the effective strategies are:

First, lock in material early. If your design requires specialty laminates (Megtron, Rogers, high-Tg polyimide), communicate your material needs to your manufacturer 4-6 weeks before you intend to release Gerbers. This allows them to secure material against confirmed demand rather than spot-buying when you place the order.

Second, consider advance scheduling. For production runs in Q3/Q4 2026, booking a production slot 2-3 weeks ahead of your need date provides scheduling certainty that is worth more than a 5% cost difference from shopping for the cheapest quote at the last moment.

Third, evaluate whether your design truly requires the advanced capabilities that are under pressure. Many boards specified with HDI or high-layer-count could be redesigned with conventional through-hole technology at lower cost and better lead time. The current environment rewards designs that are manufacturable on widely available equipment.

The Bigger Picture: Market Bifurcation

The China electronics manufacturing boom of 2025-2026 is accelerating a structural shift in the PCB industry that was already underway: the separation of the market into commodity fabrication (standard boards, price-driven, ample capacity) and advanced fabrication (HDI, RF, rigid-flex, high-layer-count — capacity-constrained, engineering-driven, relationship-dependent).

For engineers building advanced hardware, the implication is clear: your PCB manufacturer relationship is now a competitive advantage, not a commodity procurement decision. The ability to access capacity for complex boards on predictable timelines — while competitors wait in scheduling queues — directly affects your product development velocity.

ATLASPCB

Secure Your Supply Chain Partner

We maintain dedicated capacity pools for international engineering customers, with transparent pricing and committed lead times. Start with a quote to establish your manufacturing relationship.

Get Instant Quote ›Reviewed by AtlasPCB Engineering Team — 15+ years in advanced PCB fabrication for RF, HDI, and rigid-flex applications.

Related Reading:

About AtlasPCB — We specialize in complex PCB manufacturing for HDI, RF, and high-reliability applications. Explore our instant online PCB quote . Every order includes free engineering review. Get your quote.

Reviewed by AtlasPCB Engineering Team — IPC-certified manufacturing specialists with 15+ years of production experience in HDI, RF, and high-reliability PCB fabrication. Content based on factory floor data and real customer design reviews.

- China PCB manufacturer

- PCB pricing

- electronics manufacturing

- supply chain

- PCB lead time